Quick Bite – US Q3 Earnings Watch

The good news from US third quarter reporting season keeps on coming. S&P 500 companies’ aggregate forward earnings per share rose to yet another record high during the last week of October to $299. Expectations are that the year-end level will be higher still. The Q3 earnings season is beating expectations, even after the excellent Q1 and Q2 earnings seasons, which also beat expectations.

At the start of the current earnings season, industry analysts projected an increase of just over 6%. The estimated total growth rate is over 10% at present, and for the 315 companies that have reported so far, they showed earnings +15% on revenues up +8%.

Source: The Weekly ChartStorm

Goldman Sachs’ David Kostin’s observations from the earnings season so far:

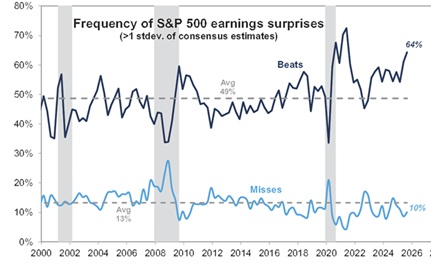

- The frequency of earnings “beats” has been unprecedented: 64% of S&P 500 companies reporting results have beaten consensus EPS forecasts by large margins. Over 25 years of data, this frequency of earnings surprises has been surpassed only during the COVID reopening period in 2020-2021.

Source: Goldman Sachs

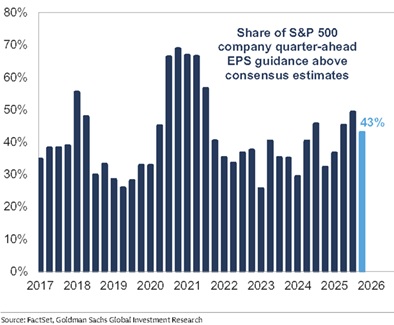

- Company guidance and analyst earnings revisions have been solid. So far, 49 companies have provided guidance for 4Q earnings. Of these, 43% have guided quarter-ahead EPS above consensus estimates, and above the quarterly average of 40% during the past decade.

Source: FactSet, GS

- Mega-cap AI capex spending continues to exceed expectations. Consensus estimates for hyperscaler capex spending in 2026 have risen from $314 billion at the start of the year, to $458 billion at the start of the earnings season, to $518 billion today. Current consensus estimates show the hyperscalers boosting capex spending by 29% in 2026, compared with an estimate of 19% expected at the start of the reporting season.

- The post-earnings share price performance of the mega-cap tech stocks reporting this week suggests investor willingness to accept capex spending growth is dependent on the strength of earnings growth and the perceived ability to monetize AI investments. Perhaps this is “a red flag” of too high expectations?

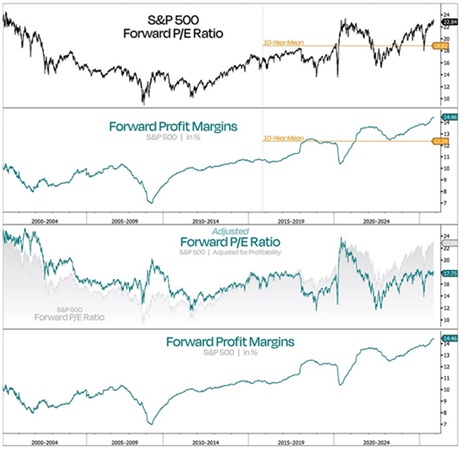

- Profit margins: the US has been outperforming the median global profit margin over the past decade (which helps explain the US vs global stocks relative stock price outperformance). Second, global profit margins have been turning up off the 2024 lows, helping explain the better performance from global stocks over the past year.

Source: Topdown Charts, LSEG

- This shows how extraordinary the current run in US profit margins is both vs history and vs the global experience. But note that issues around “circular funding” in the AI space may prompt some to wonder about the sustainability of the current surge in US profit margins (especially given how profit margins tend to be both cyclical and mean reverting).

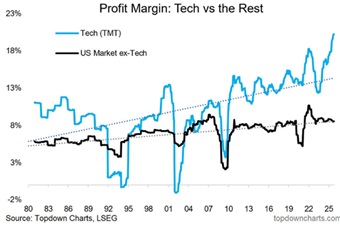

Now let’s put the focus on US tech profit margins, which are truly extraordinary!

Source: Topdown Charts Professional

Is it any wonder that the mega tech companies have rallied so hard? How long can this continue?