Quick Bite –IMF reports on Global Economic Outlook

The IMF has released its October edition of the World Economic Outlook. According to the IMF, the global economy is adjusting reasonably well to a landscape reshaped by new policy measures. Some extremes of higher tariffs were tempered, thanks to subsequent deals and resets. But the overall environment remains volatile, and temporary factors that supported activity in the first half of 2025—such as front-loading—are fading.

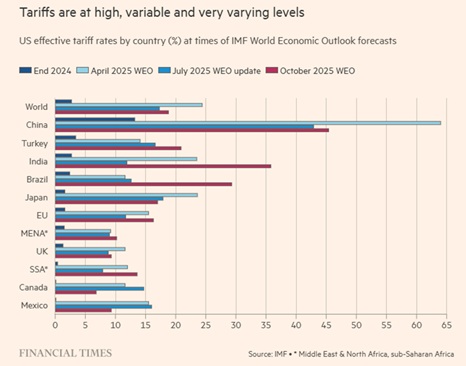

Source: Financial Times

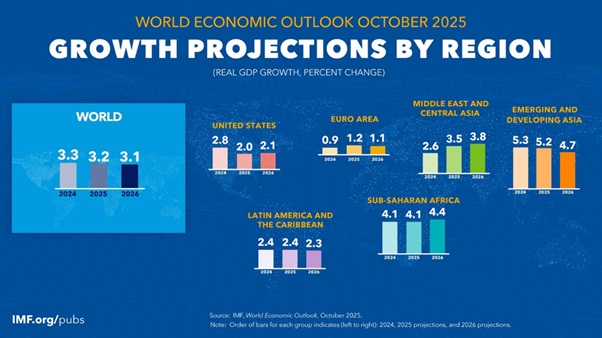

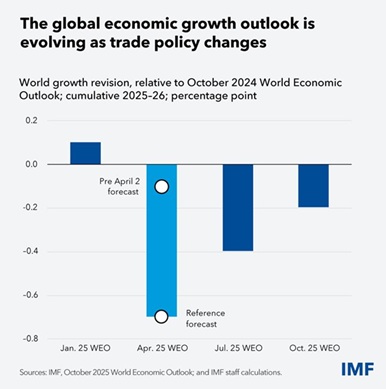

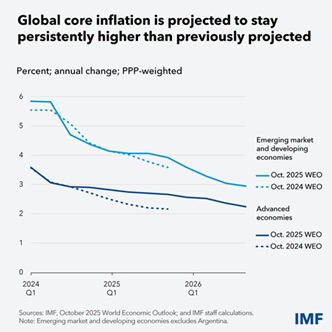

As a result, global growth projections in the latest World Economic Outlook (WEO) are revised upward compared to the April 2025 WEO but continue to mark a downward revision relative to the pre-policy-shift forecasts. Global growth is projected to slow from 3.3% in 2024 to 3.2% in 2025 and 3.1% in 2026, with advanced economies growing around 1.5% and emerging market and developing economies just above 4%. Inflation is projected to continue to decline globally, though with variation across countries: above target in the United States (with risks tilted to the upside) and subdued elsewhere.

But risks are noted. Prolonged uncertainty, more protectionism, and labour supply shocks could reduce growth. Fiscal vulnerabilities, potential financial market corrections, and erosion of institutions could threaten stability.

Source: IMF

The good news is that the growth downgrade in the forecast is at the modest end. The reasons are clear: the US negotiated trade deals with various countries and provided multiple exemptions. Most countries refrained from retaliation, keeping instead the trading system largely open. The private sector also proved agile, front-loading imports and speedily re-routing supply chains. As a result, the increase in tariffs and its effect has been smaller than expected so far.

Source: FT

However, we should not start celebrating just yet. Experience suggests that it may take a long time before the full picture appears. So far, the incidence of the tariffs seems to fall squarely on US importers, with import prices (excluding tariffs) mostly unchanged, and limited retail price increases. But they may still pass costs onto US consumers, as some have started to do, and trade may reroute permanently, leading to global efficiency losses.

Source: IMF

Furthermore, while central banks are in rate-cutting mood, inflation may prove stickier than expected.

Source: IMF

The IMF highlighted several risks apart from the threat of sticky inflation.

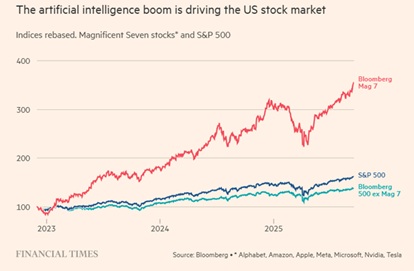

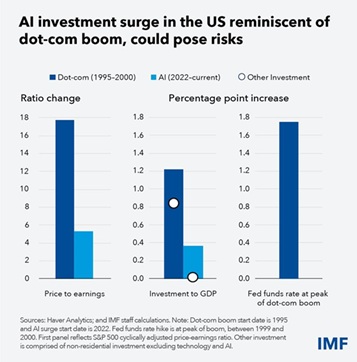

- The AI surge, promise or peril?

The IMF notes that today’s surging investment in artificial intelligence echoes the dot-com boom of the late 1990s. Optimism is fueling tech investment, lifting stock valuations, and boosting consumption via capital gains. This could push the real neutral interest rate upwards. Continued exuberance may require tighter monetary policy just as in the late 1990s.

But there is also a flip side. Markets could reprice sharply, especially if AI does not justify lofty profit expectations. That would dent wealth and curb consumption, with adverse effects potentially reverberating through the financial system.

Source: FT

Source: IMF

- China’s structural struggles

The outlook stays worrisome in China, where the property sector is still on shaky ground 4 years after its property bubble burst. Financial stability risks are elevated and rising as real estate investment continues to contract, overall credit demand is still weak, and the economy teeters on the edge of a debt-deflation trap. Manufacturing exports have buoyed growth, but it is hard to see how this could last.

Even the pivot toward investment in new strategic sectors such as electric vehicles and solar panels through use of large-scale subsidies, while boosting productivity in these sectors, may have contributed to a significant misallocation of resources and lacklustre productivity gains. Industrial policy can help boost production in targeted sectors but should be handled with care as it often brings significant hidden costs and potential spillovers.

- Mounting fiscal pressures

Many governments, including some major advanced economies, face growing fiscal strains and have achieved only limited progress in rebuilding fiscal space. Without immediate action, slower economic growth, higher real interest rates, coupled with elevated debt and new spending needs (particularly for defense, economic security, and the climate threat) will further reduce fiscal options. Low-income countries are especially vulnerable, as they face reduced aid flows. Limited opportunities could fuel social unrest, particularly among unemployed youth.

- Institutional credibility at risk

As fiscal constraints become more binding, many institutions face rising political pressure. For central banks, pressures to ease monetary policy, whether to support the economy at the expense of price stability, or to lower debt servicing costs, are ramping up. But while they may lower real interest rates in the short term, inflation and inflation expectations ultimately could flare up in response. Trust in central banks helps anchor inflation expectations—especially amid shocks. As independence erodes, decades of hard-won credibility could vanish, endangering macroeconomic and financial stability.

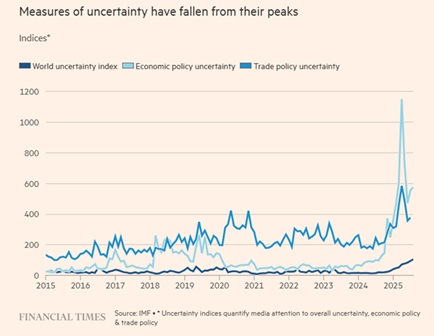

Needless to say, there is a high degree of uncertainty – especially with global economic forecasts. And yet market measures of uncertainty have trended down in recent months. Perhaps this reflects excessive optimism – the truth is that no one really knows for certain.

Source: FT