Quick Bite –AI investment going over the top

The ongoing boom in investment in artificial intelligence (AI) might be entering an increasingly perilous phase, fundamentally altering the landscape of investment risk.

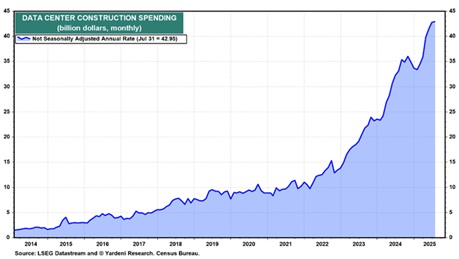

Data Centre Construction Spending

Source: Ed Yardeni

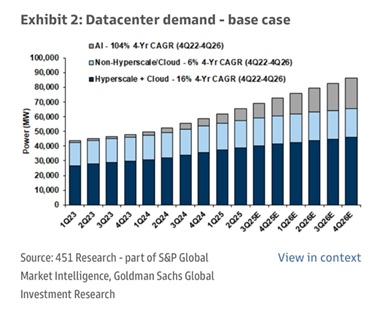

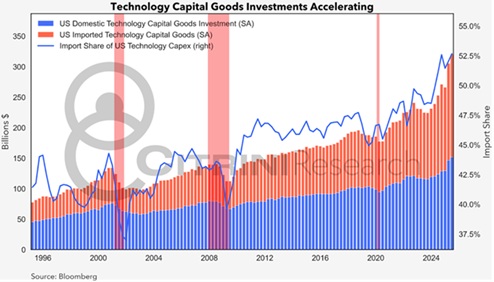

Initially driven by “hyperscalers” (companies that operate massive, globally distributed data centres to provide highly scalable cloud computing services, like Amazon Web Services, Microsoft Azure, and Google Cloud), who financed their expansion through substantial internal cash reserves, the sector is now pivoting toward more complex, leveraged, and often opaque financing mechanisms. This shift is driven by the escalating capital requirements for developing and deploying generative AI, with global data centre spending forecast to approach $3 trillion by 2029, as per Morgan Stanley.

Source: Goldman Sachs

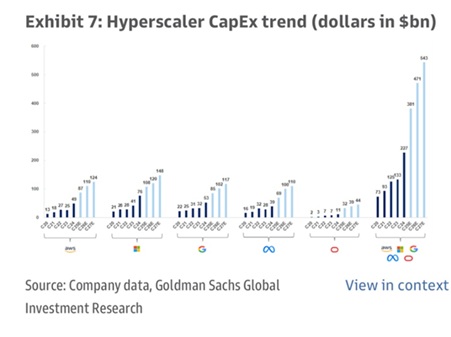

Major technology firms remain key investors, yet their internal funding sources are becoming insufficient for the scale of infrastructure investments needed. Consequently, they are increasingly turning to public and private credit markets, securing significant debt, e.g. Meta’s recent $29 billion raise, predominantly through debt instruments, to fund new data centre projects. This growing reliance on debt extends beyond investment-grade entities, encompassing non-investment-grade borrowers such as OpenAI, and other AI start-ups, broadening the spectrum of associated financial risks.

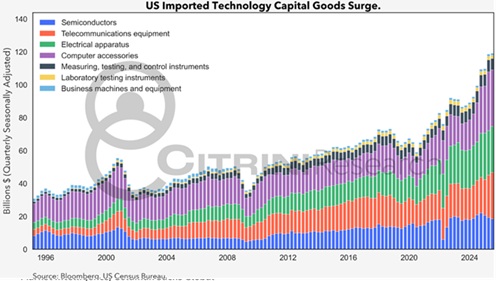

Source: Bloomberg, US Census Bureau

Last month, OpenAI committed to purchasing 6 gigawatts worth of AMD’s chips, starting with the MI450 chip next year. The ChatGPT maker will buy the chips either directly or through its cloud computing partners.

Others are building at pace too. Elon Musk’s xAI has built Colossus 1, a data centre with 200,000 Nvidia chips, and is building Colossus 2, which is expected to be even bigger. Both are in Memphis and will be powered by an electrical plant that xAI is also building. All of this is being done to have the computer capacity to train xAI’s Grok.

CEO Mark Zuckerberg says Meta Platforms will invest $65 billion into AI, mostly to build data centres this year. One of his projects in northern Louisiana is a 4 million-square-foot data centre with two gigawatts of computing power that’s expected to cost $10 billion.

In Indiana, Amazon is building around 30 data centres, which will consume 2.2 gigawatts of electricity. It is expected to serve a single customer, AI startup Anthropic (creator of Claude AI), in which Amazon has invested $8 billion. It’s part of Amazon’s Project Rainier, which will also include facilities in Mississippi and possibly North Carolina and Pennsylvania.

Source: Goldman Sachs

Microsoft plans on spending $7 billion on its Fairwater project in Wisconsin, which will include 1.2 million square feet of space. Two months ago, Google announced the start of a data centre project in Memphis that will involve $4 billion of investment through 2027. Overall, the company has said it will spend $25 billion over the next two years on data centres and AI infrastructure.

How High is Too High?

Source: Yardeni Research

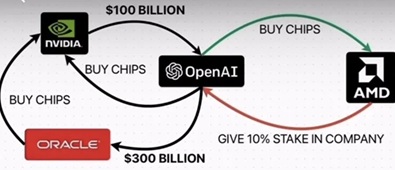

A notable feature of this evolving landscape is the proliferation of complex circular financing arrangements within the tech supply chain. These involve interdependent agreements with major semiconductor manufacturers, cloud service providers, and infrastructure developers, creating a dense web of exposures that are difficult to untangle and regulate effectively. For example, OpenAI has executed over $1 trillion worth of deals with Nvidia, Oracle, AMD, Broadcom, and others, often involving layered and circular funding structures that amplify systemic vulnerabilities.

I know, it’s hard to explain…

Source: John Rubino

The implications of this shifting financial architecture are significant. While the stock market remains alert to valuation bubbles (discussed in a recent QB published on 14 October “Are we in a stock market bubble?”) prompting warnings from the IMF about tech valuations reminiscent of the dotcom era, the increasing debt burden introduces a new layer of risk. Defaults could cascade through both banking and non-bank sectors, especially if revenue generation from AI initiatives fails to meet expectations. The reliance on lower-quality debt raises the likelihood of defaults, which could trigger broader financial contagions.

Source: Bloomberg

From a technological standpoint, the sustainability of this investment binge hinges on the economic viability of AI applications. Although ChatGPT has achieved widespread consumer adoption, scaling enterprise solutions and realizing productivity gains at a macroeconomic level will take time. Inadequate returns or unforeseen technological obsolescence, such as rapid chip innovation or high electricity costs, pose additional threats.

Historically, over-investment in infrastructure can yield long-term benefits, as seen with 19th-century railways and dotcom-era fibre networks. Excess capacity eventually supports new growth cycles, suggesting that, even if overzealous, current AI infrastructure could underpin future innovation.

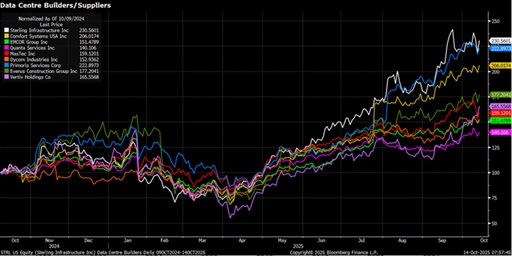

Data Centre Builders and Suppliers on a Tear

Source: Evans and Partners

Ultimately, the AI-driven data centre expansion and other capital intensive investment in AI capabilities could transcend productivity gains, evolving into a stress test for financial stability. The entanglement of credit, capital, and confidence warrants heightened corporate discipline, investor scrutiny, and regulatory oversight. A misstep could reverberate beyond technology valuations, challenging the resilience of highly priced financial markets.