Quick Bite – Coming for Dr Copper

Copper is nicknamed “Dr Copper” because its widespread use in industries like construction, manufacturing, and energy makes its price a strong leading indicator for the health of the global economy. When demand for copper rises, it suggests economic expansion, while falling demand can signal an economic slowdown, acting like a diagnostic tool for the economy’s “health”.

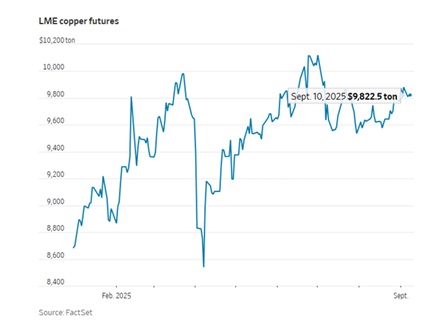

Source: FactSet

Copper has long been regarded as a cornerstone of the global energy transition. Its role in wind turbines, solar farms, electric vehicles (EVs) and power grid infrastructure has underpinned a steadily rising demand profile. However, the metal is now also riding two additional megatrends: artificial intelligence (AI) and increasing global military expenditure – both of which are poised to add further strain to a market already facing supply bottlenecks.

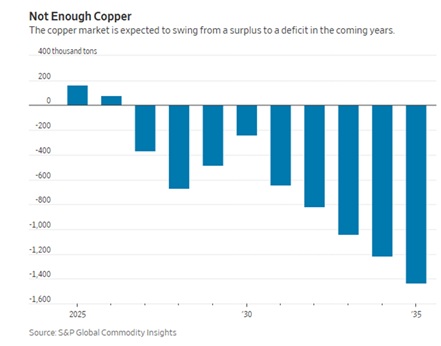

Source: S&P Global Commodity Insights

Expanding Sources of Demand

The green transition remains the primary structural driver. EVs alone are expected to push copper demand from 1.3 million tons in 2025 to 2.3 million tons by 2030, while requirements for upgrading and expanding electricity generation and transmission networks are forecast to rise 19% to 14.9 million tons over the same period. Major producers expect overall demand to grow by around 70% by 2050.

AI is adding a new layer to this demand profile. Data centres built to support machine learning workloads are highly copper-intensive, with significant requirements for wiring, cooling, and power systems. Over the next decade, data centres are projected to consume more than 4.3 million metric tons of copper, nearly equivalent to a year’s supply from Chile, the world’s largest supplier. This incremental demand introduces a structural shift that the market has only recently begun to price in.

Military rearmament provides a third source of demand. Copper is integral to weapons systems, vehicles, and ammunition. If global defense spending were to rise from the current 2.5% of GDP toward 4% (equal to levels seen before the end of the Cold War), annual demand would increase by approximately 170,000 tons. This may appear small relative to total global use, but in a finely balanced market it represents a meaningful increment.

Supply Constraints and Industry Response

On the supply side, challenges are persistent. Large-scale mines take decades to bring online, with regulatory hurdles and local opposition delaying projects even in politically stable jurisdictions. A proposed mine in Arizona has been under development for roughly two decades without resolution. Against this backdrop, consolidation in the mining sector has accelerated as producers seek to acquire rather than build assets.

A proposed $53 billion merger of Anglo American and Teck Resources announced last week would create one of the world’s five largest copper producers, with a diversified base in Chile, Peru and Canada. This highlights the scarcity value of established low-risk copper operations.

Price Dynamics and Outlook

Copper prices currently sit around $9,800 per ton (or around $4.50 per troy ounce), up from lower levels earlier in 2025 despite volatility driven by trade policy and tariffs. Forecasts suggest prices could average around $11,500 per ton in 2026–27. The combination of accelerating demand, structural supply challenges, and geopolitical risk underpins a bullish medium-term trajectory.

Of course, as with most commodity markets, short-term fluctuations are likely as policy shifts, tariff announcements, and macroeconomic sentiment interact with the physical market, but the underlying fundamentals remain supportive.

Investment Implications

For investors, copper’s story is no longer just about green energy. The convergence of AI infrastructure build-out, rearmament cycles, and electrification trends points to sustained upward pressure on prices. While substitutes such as advanced superconducting wires are emerging, they remain niche and will not materially offset copper demand in the coming decade. In this context, producers with scalable, low-cost copper assets are positioned to benefit disproportionately, while broader commodity exposure offers a hedge against energy transition and geopolitical uncertainty.

As nations vie for access to limited future copper supplies, securing domestic or friendly sourcing and refining capabilities are emerging as a strategic geopolitical imperative.